House prices remained broadly flat in April as higher borrowing costs and renewed economic uncertainty weighed on buyer confidence according to the latest Halifax House Price Index.

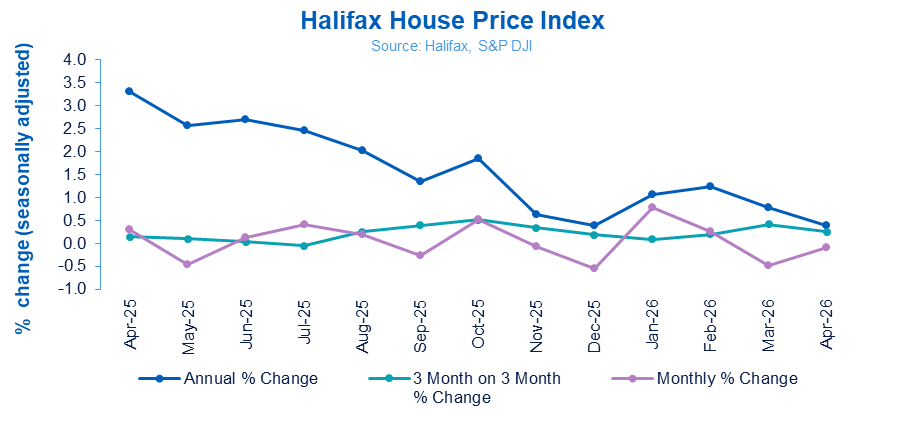

The lender said average UK property prices dipped by -0.1% during the month, following a -0.5% decline in March, leaving the average home valued at £299,313.

Annual house price growth also slowed to +0.4%, down from +0.8% the previous month, as lenders and borrowers continue to grapple with increased volatility in swap rates and mortgage pricing.

The figures suggest the market is entering a more cautious phase after a relatively resilient start to 2026, with affordability pressures once again becoming a key issue for borrowers and brokers alike.

LITTLE MOVEMENT

Amanda Bryden (main picture, inset), head of mortgages at Halifax, said: “Average house prices showed little movement in April, edging down by just -0.1% compared to March, with the typical property now costing £299,313. The pace of annual growth also eased to +0.4%.”

She said recent global developments and higher energy prices had increased uncertainty around inflation and interest rates, adding that markets had “reassessed the path for interest rates”, pushing up borrowing costs for many buyers.

Bryden added that while the housing market was likely to cool in the near term, wage growth continuing to outpace house price inflation was helping to support overall stability.

AFFORDABILITY CHALLENGE

The data is likely to reinforce expectations that affordability will remain a central challenge for advisers throughout the second half of the year, particularly for first-time buyers facing elevated mortgage rates alongside higher living costs.

Halifax said the average price paid by a first-time buyer fell slightly to £238,908, its lowest level so far this year.

Regional performance continued to show a clear North-South divide.

Northern Ireland recorded the strongest annual growth at +7.6%, with average prices reaching £224,851, while Scotland posted annual growth of +4.0% to £222,448.

In England, the North East recorded annual growth of +4.5%, while the North West saw prices rise +3.4%.

By contrast, southern markets remained under pressure. The South East recorded the largest annual decline at -2.0%, while London prices fell -1.4% year-on-year to £536,051.

BARELY MOVING

Joe Nellis is economic adviser at MHA, the accountancy and advisory firm, said: “The latest Halifax HPI report points to a housing market that is barely moving. Annual growth is now at only 0.4%, half the 0.8% recorded in March. This is a market that has stabilised, but only at a low growth rate.

“This should be good for affordability, but rising inflation and financing costs are having an opposing effect. Mortgage rates have been edging upwards as conflict in the Middle East has unsettled financial markets and threatened a hike in interest rates, and inflation is set to eat into purchasing power.”

“This puts potential house buyers in a bind.”

He added: “This puts potential house buyers in a bind. Do they look to buy now while house price growth remains low, and before interest rates potentially rise? Low demand in the economy makes interest rates going upwards an unlikely scenario, but one that cannot be ruled out.

“Alternatively, do they hold their nerve, waiting for interest rates to fall but risking prices picking up pace again?”

INDUSTRY REACTION

Tomer Aboody, director of specialist lender MT Finance, said: “The housing market saw a small bounce at the end of last year and at the start of this one once the Budget was out of the way as buyers and sellers felt more confident about their prospects.

“Since then, market conditions have become more difficult, with hope of lower base rate and stamp duty concessions dwindling. However, many have come to the conclusion that they have waited long enough to move and now simply have to because of their situation, regardless of what is going on in the Middle East and the pressure that is placing on the economy.”

FIRST-TIME BUYER BOOST

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “Although UK gilts, which are intrinsically linked to Swap rates which impact the pricing of mortgages, hit multi-decade highs as UK political and inflation risks mount, mortgage rates are now falling as lenders trim rates.

“Given that mortgage rates surged in March, buyers who need to move may be seizing the opportunity to grasp cheaper deals while they can. Affordability remains under pressure, however, with buyers negotiating hard.

“First-time buyers will be encouraged as house prices remain steady rather than soar. Lenders are working hard on offering solutions to those trying to get on the ladder for the first time, which is leading to an improvement in their numbers.”

THE NEW NORMAL

Jeremy Leaf, north London estate agent and a former RICS residential chairman, said: “These historically-reliable figures confirm much of what we are seeing in our offices – housing market activity may not be what it was just a few months ago, when it was growing steadily, but buyers and sellers are coming to terms with a ‘new normal’ of uncertainty with regard to mortgage rates and inflation.

“We are finding it is harder to gain commitment with so much choice of property as buyers negotiate hard and try to convince themselves that they are still getting value for money.”

ECONOMIC OUTLOOK

Karen Noye, mortgage expert at Quilter, said: “The monthly move is less important than the fact the market is still having to price homes against a rapidly shifting interest-rate backdrop, and the Bank of England’s decision to hold the Bank Rate at 3.75% last week did not close down the risk of higher borrowing costs.

“The recent shift in tone around US-Iran talks is therefore significant for the housing market. If a credible peace deal is brokered and oil prices continue to ease, the case for further UK rate rises becomes harder to sustain. Swap rates would be expected to stabilise and potentially move lower, giving lenders more scope to trim fixed mortgage pricing.

“That would not transform affordability overnight, but it would remove one of the biggest sources of uncertainty facing buyers. A market that has been subdued due to caution could find some support if households can see a clearer path for mortgage rates.

“If energy prices settle and swap rates drift lower, mortgage lenders are likely to compete harder for borrowers. If the conflict escalates again, the risk is that recent mortgage rate improvements unwind quickly.”