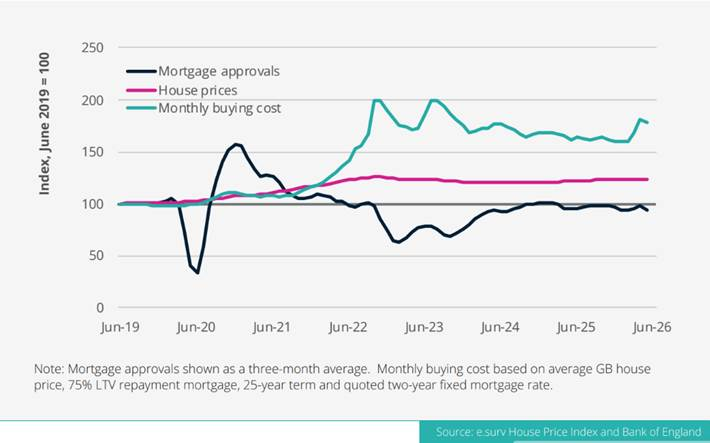

The cost of buying a home has risen more than three times faster than house prices since 2019, leaving borrowers increasingly constrained by affordability despite continued resilience in buyer demand.

The latest House Price Index from e.surv found the average house price across Great Britain has increased by around 24% over the past seven years to £328,800.

Over the same period, however, the indicative monthly cost of buying the average home has climbed by approximately 78%.

While mortgage approvals have recovered from the interest rate shocks of 2022 and 2023, activity has yet to return to pre-pandemic levels. On a rolling three-month basis, mortgage approvals in May were around 6% lower than in June 2019.

The Bank of England has reduced Bank Rate to 3.75% over the past year and average fixed mortgage pricing has eased, but borrowing costs remain well above the ultra-low levels that underpinned the housing market before 2022.

The findings suggest the housing market remains active but increasingly price sensitive, with buyers placing greater emphasis on affordability as higher borrowing costs continue to influence purchasing decisions.

AFFORDABILITY PRESSURES

Rob Owens, head of research at e.surv, said: “The gap between house price growth and buying costs helps explain much of the market’s recent behaviour.

“The impact is being felt through affordability rather than activity, with buyers increasingly constrained by borrowing costs and therefore more selective on price.

“Properties that are closely aligned to local budgets continue to attract interest, while those that stretch affordability are more likely to see longer selling times or price adjustments.

“Looking ahead to the second half of 2026, house price growth is likely to remain modest and mortgage rates have started to edge lower, which should help buyer confidence.

“Affordability pressures remain, but a more stable rate environment would give buyers and sellers greater confidence.”