Buy-to-let mortgage rates have risen sharply this month, while landlords are also facing further costs linked to planned rental sector reforms and tougher energy efficiency requirements.

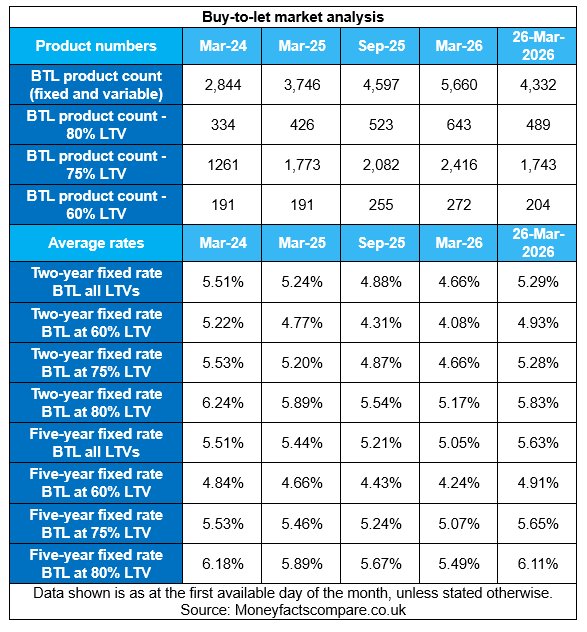

Research from Moneyfactscompare.co.uk suggests average fixed rates on both two-year and five-year buy-to-let mortgages have increased since the start of March 2026, with product choice also falling significantly.

The average two-year fixed buy-to-let rate is now at its highest level for a year, last seen at 5.40% in February 2025. The average five-year fixed rate has reached its highest point for two years, last seen at 5.91% in January 2024.

Moneyfacts said borrowing costs for landlords taking out a two-year fixed deal are now around £1,100 a year higher than at the start of March, based on a £250,000 loan over a 25-year term.

The data also showed that overall buy-to-let product availability, across fixed and variable deals, has fallen by about 1,300 products since the start of the month. Choice was last below 5,000 deals in November 2025.

The findings come as landlords prepare for further regulatory and financial pressures. Moneyfacts said the Renters’ Rights Bill is due to come into effect at the start of May 2026, while landlords are also expected to spend up to £10,000 to bring properties up to an EPC rating of C by October 2030, subject to property value.

Rachel Springall, finance spokesperson at Moneyfactscompare.co.uk, said: “Soaring borrowing costs will cause pain to landlords this year, as they join millions of consumers facing higher mortgage repayments.

“This is terrible news, as rising costs could lead to higher rental payments for tenants, or a drop in the pool of properties available for rent if landlords decide enough is enough and sell off their portfolio.

“The unrest in the Middle East has caused absolute mayhem in the residential mortgage market, buy-to-let rates are also being hiked, and hundreds of deals have been pulled from sale.”

She said: “The positive sentiment entering 2026 has been shattered, and landlords not only have to face higher borrowing costs, but also prepare themselves for the Renters’ Rights Bill, which comes into effect at the start of May 2026.

“Those who were to take out a mortgage now compared to the start of this month will face higher repayments of £1,100 more a year. This is based on a borrowing of £250,000, over 25 years at 5.29%, versus 4.66% at the start of March 2026.”

Springall said landlords may also need to consider further borrowing to cover improvement works required under the proposed changes and wider housing standards.

She said: “It is entirely possible that landlords may have to take on an additional loan to cover refurbishment costs, to ensure they abide by the Decent Homes Standard, which is set out in the Renters’ Rights Bill.

“It is of course essential that tenants feel safe and secure in their homes, and it will be ever more essential to have a dwelling as energy-efficient as possible with rising costs expected this summer.

“Thankfully, lots of progress would have been made to make private lets more energy-efficient over the past six years, under the Minimum Energy Efficiency Standard (MEES) regulations, whereby landlords have been prohibited from letting properties with an EPC rating below E.

“However, landlords’ costs will escalate further, as they are expected to invest up to £10,000 as a spending cap to reach an EPC rating of C by October 2030, subject to the value of a property.

“If that EPC rating is not achieved, landlords could face substantial fines, as the rules apply to all tenancies. Seeking advice will be essential for new or existing landlords to keep on top of the changing legislation and how rising costs and interest rate rises will hit their profit margins.”