There was a further fall in the number of mortgages in arrears, as well as the number of repossessions, in the third quarter of the year.

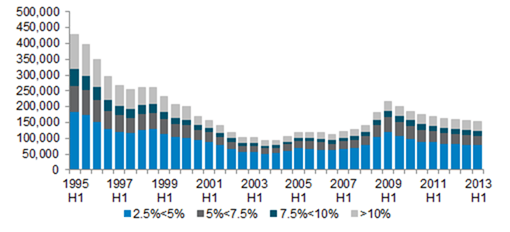

The latest survey results from the Council of Mortgage Lenders shows the proportion (and number) of borrowers behind with their payments fell across each of the arrears bands. A total of 149,400 mortgages, representing 1.33% of the entire stock of mortgages, had arrears equivalent to more than 2.5% of their mortgage balance at the end of the third quarter. This was down from 154,900 (1.38%) in the second quarter, and 159,100 (1.4%) in the third quarter of 2012.

Arrears on mortgages, by percentage of total balance in arrears

Source: CML Research

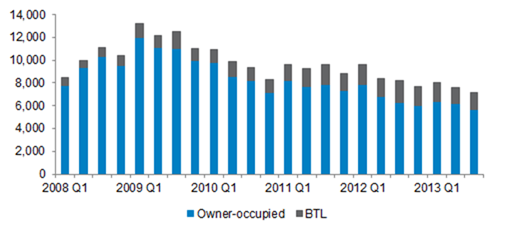

The repossession rate also fell from 0.07% in the third quarter to 0.06% in the fourth quarter, its lowest level since the CML began publishing quarterly data at the beginning of 2008. At 7,200, the quarterly number of repossessions was also the lowest since quarterly data began – down from 7,600 in the second quarter and 8,200 in the third quarter of last year.

The CML figures cover both home-owner and buy-to-let arrears and repossessions. Arrears in the buy-to-let market are lower than in the home-owner market. While buy-to-let mortgages represent over 13% of the total number of mortgages in the UK, the sector accounts for only 9% of the total number of mortgages in arrears. However, the repossession rate is a little higher on buy-to-let than on home-owner mortgages (0.10% on buy-to-let compared with 0.06% on home-owner-mortgages). Of the 7,200 total repossessions, 1,500 were buy-to-let.

Repossessions, buy-to-let and owner occupied markets

Source: CML Research

Overall, the total number of repossessions for the full year now looks likely to be fewer than 30,000, compared with the CML’s start of year forecast of 35,000. And the CML’s current forecast of 37,000 repossessions in 2014 will also be revised downward when the CML housing market forecasts for next year are published in December.

CML director general Paul Smee said: “The continued reduction in payment difficulties is obviously very welcome. Anyone who does face the prospect of difficulty can be reassured that repossession really is a last resort. By talking to their lender as soon as possible, most can resolve their temporary problems, without the lender resorting to repossession. It also makes sense for people to think ahead now to how they will manage their finances to cope with higher interest rates, and higher mortgage payments, as and when rates rise in the future.

“As the Government’s mortgage rescue scheme in the English regions closes to applications at the end of March next year, we will be sorry to see it go. While the 5,000 households helped directly through mortgage rescue may seem relatively small, the benefit to those households was huge. And the scheme played a vital role in encouraging borrowers to talk to their lender, and seek free independent debt advice. Lenders remain fully committed to helping their borrowers as far as realistically possible to manage arrears if they do arise, and get back on track.”