Financial markets could be overreacting in the early days of the conflict as they take a second rate cut off the table this year.

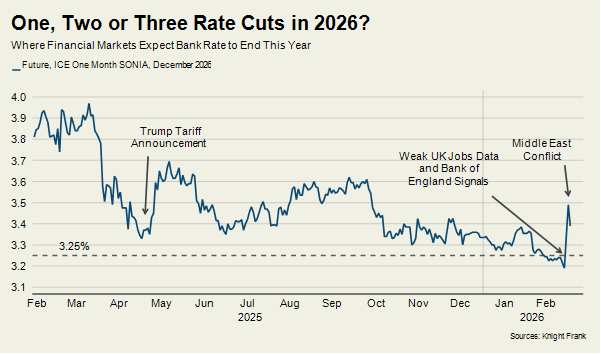

The conflict in the Middle East and accompanying spike in energy prices means financial markets expect fewer rate cuts from the Bank of England this year.

That was the position on Thursday this week, although events have been unfolding quickly since the war started less than seven days ago.

Higher borrowing costs would undermine housing market activity, but traders may have overreacted, according to Michael Brown, research analyst at Pepperstone, speaking on the latest episode of Knight Frank’s Housing Unpacked podcast.

“The two-year swap is at its highest level since November, and the five-year swap is the highest it has been since January,” he said. “I think the market has lurched too far in one direction and will probably slowly but surely lurch back in the other.”

Swap prices, which are based on future rate expectations, are used to price fixed-rate mortgages.

Soft employment figures and strong signals from the Bank of England about inflation coming under control meant a March cut felt almost certain this time last week. A second cut was also priced in before December, which would have taken Bank Rate to 3.25%, as the chart shows.

More cuts are likely to be factored back in as the situation settles in the Middle East, said Brown.

“The market was pricing in two cuts this year and it’s now pricing in one, but I still think we’ll get three,” he said.

Three cuts would certainly help push mortgage rates closer to 3% than 4% and support demand in the housing market as it recovers from the prolonged period of uncertainty that preceded November’s Budget.

Why does Michael Brown believe the Bank of England will cut three times before December, taking Bank Rate to 3%?

“The labour market is still very weak, demand is still pretty soft in the broader economy and inflation is on its way back to the 2% target, even if we have a little bit of a blip.

“For markets to price back in two or more cuts, the first thing we need to see is energy prices coming back down. The second is more data of the kind we were getting earlier this year, pointing to a soft labour market and relatively anaemic growth.”

SAFE HAVENS

We also discuss which safe havens investors are seeking against the backdrop of the military conflict and how a prolonged war in the Middle East could affect sentiment more widely among buyers.

Geopolitical events certainly helped Chancellor Rachel Reeves in her aim of making the Spring Statement a non-event this week.

However, many of the assumptions underlying the economic forecasts made by the Office for Budget Responsibility (OBR) are now out of date thanks to the market shifts since the Iran conflict began.

The movements could reduce her financial headroom further and put tax hikes more firmly back on the agenda at this year’s autumn Budget.

“We’re at a point where higher taxes are going to be counterproductive because disposable incomes fall and your tax base shrinks,” said Brown. “The OBR recently cut their net migration forecast, not because fewer people are coming in but because more people are leaving.”

So, will the Chancellor try and raise taxes for the third time in 2027? Quite possibly, but who delivers the Budget is another matter.

“I don’t think it’s going to be Rachel Reeves’ third Budget in a row,” said Brown. “I think that’s actually one of the reasons she gave a relatively good address in the Commons this week, because she’s almost got nothing to lose at this point, given Keir Starmer’s rather perilous position.”