Britain’s housing market experienced its slowest month in over a year this February as the surge of buyers rushing to complete deals ahead of looming stamp duty changes began to ease.

The Royal Institution of Chartered Surveyors (RICS) UK Residential Property Survey found that several factors of uncertainty reduced momentum in the UK’s housing market last month.

Buyer demand weakened, posting a net balance reading of -14% in February. This is down from -1% in January and marks the weakest result for the survey’s gauge of buyer demand since November 2023.

STAMP DUTY CHANGES

Stamp Duty changes on April 1, where the threshold will reduce from £250,000 to £125,000, is expected to weaken market activity and is believed to have driven the slowdown.

Wider geopolitical and international economic concerns are also believed to have added to the mix of housing gloom.

Yet house prices at a national level continue to rise overall, albeit at a subdued rate.

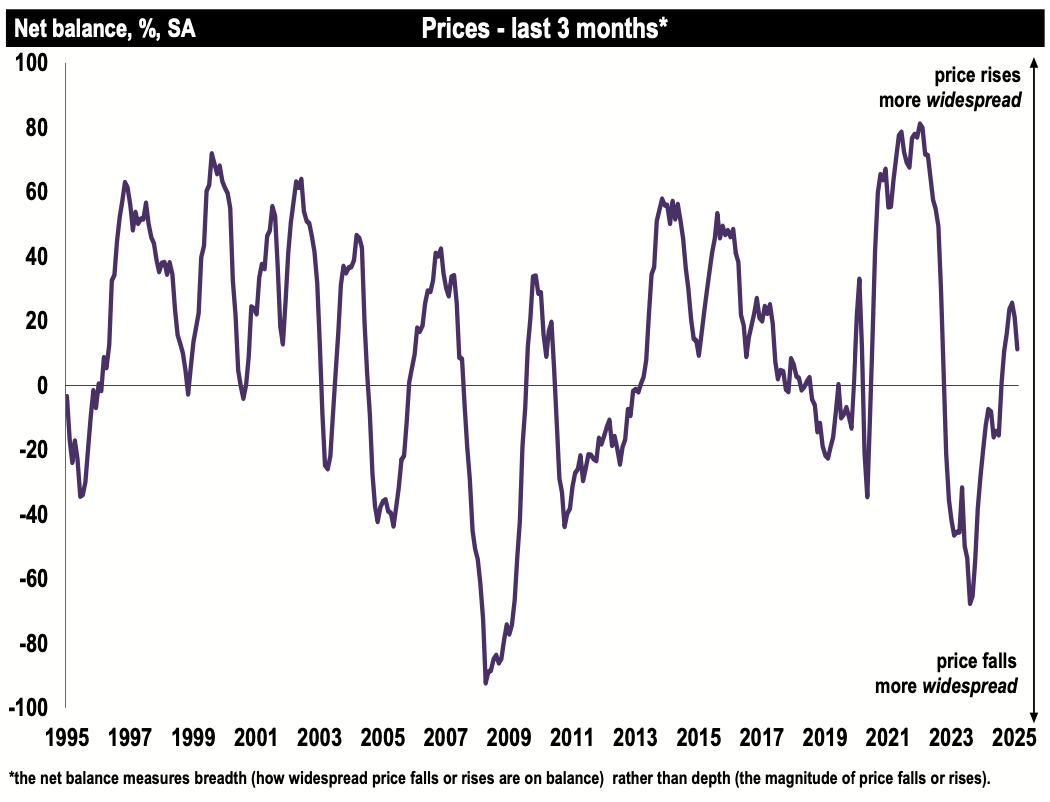

The latest net balance came for price growth came in at +11%, which remains consistent with a subtle upturn in prices.

But this has now settled in each of the last two months, easing from +25% and +21% in December and January.

And whilst the recent interest rate cut by the Bank of England was welcomed agents and surveyors are calling for more to help spark the market.

Most respondents to RICS latest survey believed that house prices will rise over the next 12 months – the net balance for the year-ahead price expectations series sits at +47%.

LETTINGS MARKET

In a blow to the buy-to-let market tenant demand recorded a figure slightly below zero for a fourth month in a row, returning a net balance of -4% in February – the longest stretch without a positive reading for this indicator since the monthly (non-seasonally adjusted) lettings dataset was established in 2012.

Simon Rubinson, RICS Chief Economist, said: “The UK housing market appears to be losing some momentum as the expiry of the temporary increase in stamp duty thresholds approaches.

“Some concerns are also being expressed by respondents about the re-emergence of inflationary pressures and the more uncertain geopolitical environment. That said, looking beyond the next few months, sales activity is seen as likely to resume an upward trend with prices also moving higher.

“A key support for the market continues to be the increased flow of existing stock becoming available, giving buyers a greater choice of options.”

CHALLENGES AHEAD

But he added: “Leading indicators around new build remain subdued for now, highlighting the significance of the Planning and Infrastructure Bill introduced to Parliament this week.

“Meanwhile, despite a flatter trend in demand for private rental properties, the key RICS metric capturing rental expectations is still pointing to further increases demonstrating that the challenge around supply spans all tenures.”

INTERVENTION NEEDED

Tomer Aboody, director of specialist lender MT Finance, said: “Although we have seen a confident market over the past 12 months as buyers make their move due to a better interest rate environment and lower inflation, both buyers and sellers have been used to much lower rates and are hoping for further cuts in coming months.

“While sales volumes are up, they are still well below historical figures and some intervention will be needed in order to inject more life into the market. Unfortunately, particularly given further difficulties ahead as the fallout from the recent Budget continues, any positive intervention doesn’t seem to be on the immediate horizon.

“In the rental market, as landlords are continually hit there is reducing availability of rental property for tenants, which is driving up rents.”